Point Predictive spots record auto fraud exposure & climbing early payment default risk

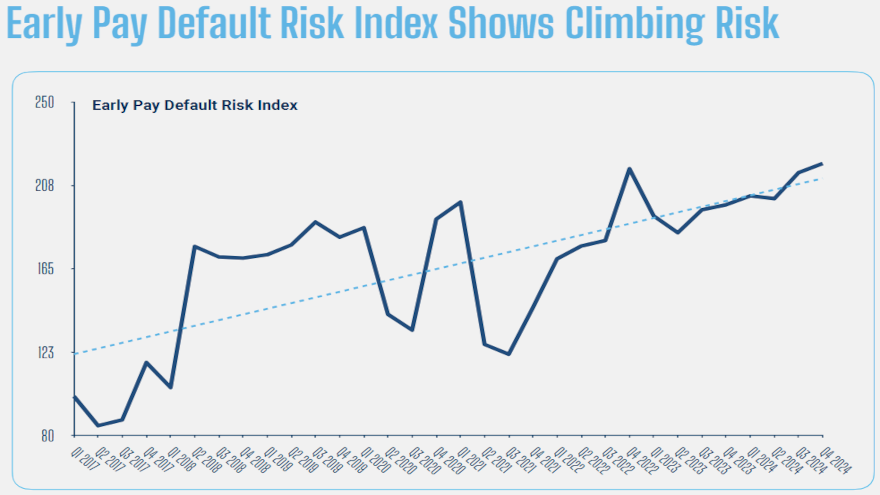

Chart courtesy of Point Predictive.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Point Predictive on Tuesday released its 2025 Auto Lending Fraud Trends Report, detailing that finance companies face an estimated $9.2 billion in fraud loss exposure for 2025 — the highest ever measured.

And another troubling metric — especially for creditors that operate in the subprime space — Point Predictive’s Early Payment Default Risk Index has increased 25% in the past 24 months.

The comprehensive report analyzing fraud patterns connected with $4 trillion in submitted loan applications revealed that first-party fraud — where consumers or dealerships misrepresent information to finance companies — accounts for 69% of the $9.2 billion fraud risk exposure that the auto-financing industry faced in 2024.

“While dramatic cases of organized crime ring stealing identities make headlines, our data reveals that the true story behind most auto lending fraud is an array of misrepresentations,” Point Predictive chief innovation officer Frank McKenna said in a news release.

“Borrowers using their own names who inflate their income, misrepresent their employment, utilize credit washing techniques, or create new credit profiles with credit profile numbers (CPNs) account for the overwhelming majority of fraud risk, yet these patterns often go undetected,” McKenna continued.

Point Predictive explained its Early Payment Default (EPD) Risk Index acts as the auto industry’s early warning system. The index tracks consumers who stop paying on their contracts within their first six months, often the strongest indicator of potential fraud or serious misrepresentation during the application process.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Up to 70% of early payment defaults contain evidence of fraud on the initial application, according to Point Predictive’s report.

Data scientists at Point Predictive analyzed performance patterns across more than 256 million loan applications and originations dating back to 2017.

“This massive dataset allows our team to identify subtle default pattern shifts that might go unnoticed,” Point Predictive said in the report. “The quarterly index establishes patterns that go beyond individual lenders’ experience to capture an industry-wide view of risk over time. By comparing default rates across different periods, the index reveals whether early payment defaults are increasing, decreasing, or shifting in nature.”

Point Predictive reported early payment defaults have more than doubled since the baseline was established in 2017, with the index climbing over 10% in 2024 alone.

Analysts noted that after a volatile period during the pandemic (2020-2021), the index began a steady climb from mid-2021 that has continued almost uninterrupted through 2024.

The latest quarterly reading shows EPD risk has increased by 10.6% since early 2024.

“Since EPD strongly correlates with fraud and misrepresentation, the index suggests that income inflation, synthetic identities, and other deceptive practices are becoming more prevalent,” Point Predictive said in the report.

Some of the revealing statistics highlighted in the report include:

—First-party fraud and misrepresentations dominate the landscape, with income and employment misrepresentation accounting for 43% of total fraud risk ($3.9 billion).

—Bust-out fraud has grown by over 26% in the last 24 months as the economy softens and more people resort to monetizing cars.

—Systematic dealer risk, such as repeatedly inflating car values and using fake employment for borrowers, increases lenders’ default risk for those dealers by as much as 500%.

The report also explores emerging threats, including the explosive growth of AI-powered fraud tools and their potential impact on lenders in 2025 and beyond.

An analysis of criminal Telegram channels revealed a 644% increase in conversations about AI and deepfakes used for fraud between 2023 and 2024, featuring sophisticated schemes such as synthetic identity generators, deepfake videos aimed at bypassing identity verification, and AI-generated counterfeit identification documents.

“This year’s report represents our largest analysis of auto lending loan data to date,” Point Predictive CEO Tim Grace said in the news release. “The extensive scale of our consortium and proprietary risk data provides us unparalleled visibility into fraud patterns that lenders’ own data simply cannot reveal.

“This data enables us to provide solutions that assist lenders in funding loans that do not contain fraud and misrepresentation while avoiding the losses associated with the array of hidden schemes that can lead to defaulted loans,” Grace went on to say.

The 2025 Auto Lending Fraud Trends Report is available via this website.