Five straight months of credit tightening for auto finance stops in September

Chart courtesy of Cox Automotive.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

While Edmunds detailed the swelling of negative equity, Cox Automotive noticed credit access loosened to close the third quarter.

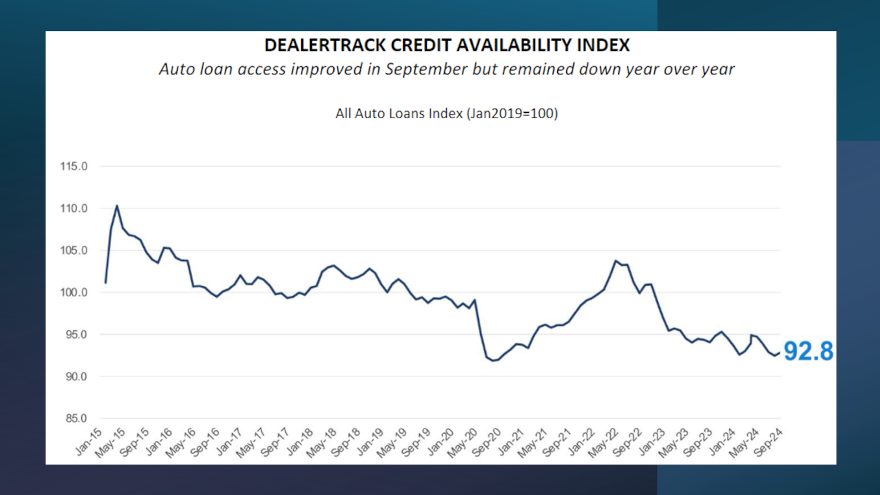

The Dealertrack Credit Availability Index came in at 92.8 in September, representing a 0.4% improvement from August and stopping a streak of five consecutive months of tightening.

However, Cox Automotive pointed out that the reading still showed credit is tighter by 2.1% year-over-year.

“The Dealertrack Credit Availability Index improved due to reduced average auto loan rates, an increased share of subprime loans and extended loan term lengths, all of which contributed to easier consumer credit access,” analysts said in a Data Point that accompanied the latest index update.

“Credit availability eased in September for all sales channels except independent used sales,” Cox Automotive continued. “Certified pre-owned loans loosened the most, while credit availability for used loans through independent dealers tightened the most but remained better than pre-pandemic levels. Overall, credit access was tighter than a year ago, with new loans showing the least tightening and certified pre-owned loans experiencing the most tightening compared to last year.

“In September, credit availability increased across all lender types,” analysts went on to say. “Credit unions and banks showed the most significant easing, while auto-focused finance companies loosened their standards the least, yet their credit availability is still tighter pre-pandemic levels. Compared to the previous year, auto-focused finance companies eased slightly, whereas banks experienced the greatest tightening.”

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Cox Automotive explained that the average yield spread on auto financing widened by 6 basis points in September, making auto rates less favorable compared to bond yields.

Analysts then pointed out the average auto rate dropped by 15 basis points from August, while the five-year U.S. Treasury fell by 21 basis points, leading to a bigger yield spread.

Perhaps what might be making consumers more interested in auto financing, Cox Automotive mentioned auto rates have dropped by 113 basis points since March.

But getting deals bought appears to still be a challenge since analysts acknowledged the approval rate decreased by 50 basis in September, sinking by 3.8 percentage points year-over-year.

Finance companies do not appear to be completely avoiding risk, since Cox Automotive noticed the subprime share ticked up for the second month in a row. Analysts said the subprime share increased by 30 basis points in September and 1.2 percentage points year-over-year.

Elsewhere in its data, Cox Automotive found that the share of contracts with terms longer than 72 months jumped by 80 basis points in September.

And reinforcing the Edmunds information, Cox Automotive noted that the number of contracts booked in September with negative equity increased 20 basis points and 1.7 percentage points year-over-year.

After being flat for three consecutive months, Cox Automotive noticed the down payment percentage fell 20 basis points in September, but it’s still 3.5 percentage points higher than a year ago.

Cox Automotive reiterated that each Dealertrack Auto Credit Index tracks shifts in approval rates, subprime share, yield spreads and contract details, including term length, negative equity, and down payments.

The index is baselined to January 2019 to provide a view of how credit access shifts over time.

Analysts closed their update by examining other economic and consumer trends.

The Conference Board Consumer Confidence Index declined 6.5% in September, when an increase had been expected, but August’s index was revised higher,” Cox Automotive said. “Consumers’ views of the present and of the future declined. Consumer confidence was down 5.4% year over year. Plans to purchase a vehicle in the next six months increased slightly compared to August but was down slightly year-over-year.

“According to the sentiment index from the University of Michigan, consumer sentiment increased 3.2% in September compared to August and was up 3.2% year-over-year,” analysts continued. “The median consumer expectation for inflation in a year declined to 2.7%, which was the lowest level since December 2020. Expectations for inflation in five years increased to 3.1%. The consumer’s view of buying conditions for vehicles improved to the best level since April.

“The daily index of consumer sentiment from Morning Consult increased 1.4% in September, extending a streak of four-monthly gains. The index was up 8.6% year-over-year,” Cox Automotive added.