TransUnion launches tools to track BNPL transactions

Screenshot courtesy of TransUnion.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

TransUnion is trying to give auto-finance companies and other lenders and service providers the clearest glimpse possible of how well consumers handle their payments and other credit obligations.

As a result, TransUnion introduced its new point-of-sale suite of solutions since analysts said up to 100 million U.S. adults have used buy now pay later (BNPL) loans at least once in the past 12 months.

TransUnion rolled out this package of tools because the credit bureau said financial institutions currently do not have access to the valuable insights generated when consumers open and repay these new debt obligations.

The company saw the urgency for these tools based on the 38% of 2,949 U.S. adults in the TransUnion Consumer Pulse study conducted in February who said they had used a BNPL loan in the last 12 months, and the U.S. Census Bureau 2020 count of 258.3 million adults living in the U.S.

TransUnion predicted inclusion of point-of-sale loans on the consumer credit file is likely to benefit the populations most in need of new tools to build and improve their credit.

Approximately 9% of point-of-sale applicants studied by TransUnion are thin file (have three or fewer trades reported). The youngest generations — Gen Z and younger millennials — will benefit as people using this credit product tend to skew younger, according to TransUnion.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Analysts also mentioned one in three point-of-sale financing applicants (33%) are between the ages of 18 and 30, compared to 17% for the overall credit-active population.

And 43% of point-of-sale applicants fall into the subprime credit risk category, compared to 13% overall, according to the TransUnion credit database that classifies subprime as someone with a VantageScore 4.0 metric within the range of 300 to 600.

“The inclusion of point-of-sale loans including BNPL into credit reports and other risk management tools can help tens of millions of consumers gain access to more credit opportunities and potentially secure better loan terms,” said Liz Pagel, senior vice president and consumer lending business leader at TransUnion.

“TransUnion has taken a measured approach in developing our solution suite, working with the top BNPL lenders over the past three years to craft solutions that benefit consumers and do not penalize them for using these products frequently,” Pagel continued in a news release.

“TransUnion’s approach helps lenders and consumers ensure credit activity is captured in a manner that maximizes benefits for consumers and to the overall credit ecosystem,” she went on to say.

TransUnion explained that point-of-sale loans are transactional, like a credit card swipe, but they are underwritten as individual unsecured installment loans. Therefore, a consumer with normal shopping habits could originate several loans per year, which most existing credit models view as risky behavior.

“This could cause undue impact to millions of consumers’ credit scores, making scores less predictive,” TransUnion said.

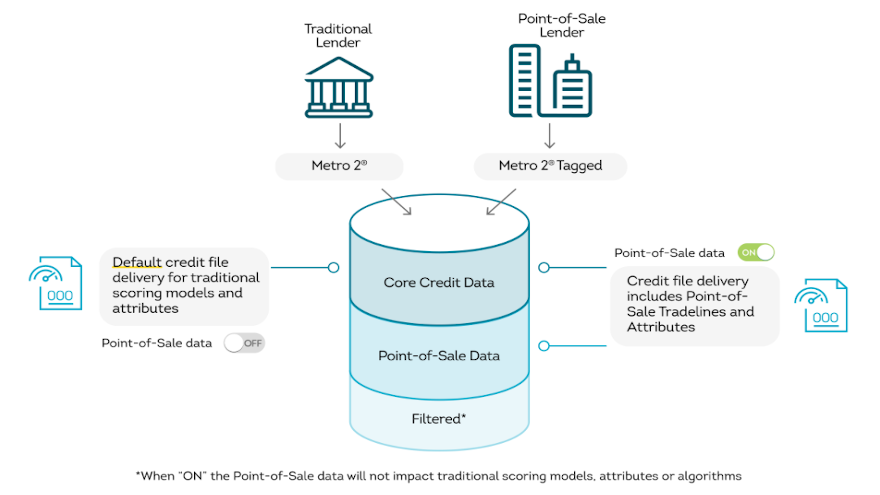

TransUnion is launching the capability to receive point-of-sale lender trades through the traditional credit reporting process, with specific Metro 2 reporting guidance that ensures FCRA compliance.

The credit bureau said the goal is to have a single standard for lenders to report data and accelerate adoption by lenders and scoring providers in the future. The information will be tagged and filtered into a new partitioned part of TransUnion’s core credit file.

Users of TransUnion credit data can choose to receive these tradelines as part of their existing credit data delivery.

Default credit report delivery, which feeds existing scoring models, will remain unaffected, according to TransUnion.

“Over time, as the industry works to enhance models with these data, it is expected that many lenders will choose to use the information in addition to their existing models to help expand their buy boxes — accelerating the consumer impact,” TransUnion said.

Long term, TransUnion highlighted that it plans on including point-of-sale data on the core credit file where it can maximize the number of credit decisions that it impacts.

“The industry needs time to adjust, and each lender will adopt the point-of-sale tradelines and attributes at its own pace,” Pagel said. “Maximizing the financial inclusion impact requires broad usage of this valuable data in more credit decisions.

Ultimately, given the prominence of FICO and VantageScore in the market, the biggest impact from the data will not be realized until the data migrates to the core file and these scores take into account consumers’ good behavior,” Pagel added.

The initial capability will allow FICO and VantageScore, along with major financial institutions, fintechs and other lenders, to have enough time to ensure that they build future versions of their underwriting models that give consumers credit for good performance on point-of-sale products.

“Buy Now Pay Later is helping many consumers access short-term credit for shopping at a time when prices are rising rapidly. BNPL can enable consumers that have not traditionally had credit records to build better credit scores,” VantageScore president and chief executive officer Silvio Tavares said in the news release.

“We think adding this data to credit scores may help drive broader financial inclusion and we are working rapidly to incorporate this into VantageScore models,” Tavares continued.

Sally Taylor is vice president and general manager of FICO Score.

“FICO is committed to financial inclusion and expanding credit access by leveraging more data, where available, and supported by empirical analysis,” Taylor said in the news release. “These are top priorities at FICO and we look forward to working with TransUnion to determine the best approach for inclusion of BNPL data in the credit file considered by the FICO Score family of products.”

More information about TransUnion’s point-of-sale suite of solutions can be found on this website.