Q3 dealer sentiment sags despite estimated double-digit rise in August used sales

Chart courtesy of Cox Automotive.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Despite a projected double-digit climb in retail used-vehicle sales in August versus July, dealers are souring on their prospects for retail success during the third quarter.

Cox Automotive compiled a variety of information connected with dealerships and their used-vehicle operations, including the newest Cox Automotive Dealer Sentiment Index (CADSI). To gauge the pace of used-vehicle deliveries, Cox Automotive leveraged a same-store set of dealerships selected to represent the country from Dealertrack.

Analysts said in a Data Point that they estimate used retail sales increased 11% in August from July but softened 9% year-over-year.

Compared to August 2019, Cox Automotive said sales were down 19%, which was an improvement from July of that year when sales were down 29%, based on the same-store results.

After sharing that retailing data, Cox Automotive reviewed estimates of used retail days’ supply based on vAuto data.

Analysts found that August ended at 47 days of supply, down from 53 days at the end of July but higher than how August 2021 when the metric landed at 38 days.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

With those data points in mind, Cox Automotive then shared that U.S. automobile dealer sentiment in the third quarter reflects that more dealers view the current market as weak than strong.

Now, at 49, the current market index is below the threshold of 50 in the Cox Automotive Dealer Sentiment Index (CADSI), marking the fifth quarter-over-quarter decline in overall market sentiment.

Analysts said in a news release that the index is down five points from Q2 and down 13 points year-over-year.

Cox Automotive noted that the current market index was last below 50 in Q1 2021; it peaked at 67 in Q2 2021.

According to research compiled for the index, U.S. auto dealers indicate that their negative view of the market is influenced by inflation, economic anxiety and tight inventory.

Cox Automotive explained the three-month, forward-looking market outlook index dropped sharply from the previous quarter and, at 44, is at a record low for the index, back to levels last seen at the onset of the pandemic in Q2 2020 and well below the 60 recorded in Q3 2021.

Analysts noted that the quarter-over-quarter decrease in market outlook, however, was driven more by independent dealers, with a 10-point drop to 40, equal to the lowest level last recorded at the start of the pandemic.

Franchised dealers’ outlook was also down quarter over quarter but by only five points, according to Cox Automotive.

More automobile dealers now view the U.S. market as weak, according to the Q3 Cox Automotive Dealer Sentiment Index.

“Importantly, a drop in current-market sentiment is not typical in the third quarter,” Cox Automotive chief economist Jonathan Smoke said in the news release. “The third quarter is usually mostly stable and, for franchised dealers, is often improving. There is typically excitement building with new models rolling out and energy for the new-vehicle market through the fourth quarter and holiday seasons. That is just not the case this year.”

Cox Automotive said the Q3 2022 CADSI research was in market from July 26 to Aug. 9, when inflation was subsiding slightly from the 40-year high in June and the Federal Reserve was raising rates again while promising more rate hikes.

Inventory continues to be sales challenge

While still historically low, Cox Automotive indicated the new-vehicle inventory level index improved from last quarter and is up significantly from one year ago.

Still, at 31, the new-vehicle inventory level index indicates inventory remains a major challenge for franchised dealers. For comparison: In Q3 2019, the index was at 61, meaning more dealers felt their inventory was growing, not declining.

“New-vehicle inventory is moving in a positive direction and clearly getting better for some dealers,” Smoke said. “But the gains are not universal. In our inventory data, we see the domestic brands are in much better shape, and the Asian brands are notably worse.”

While profits remain historically strong for franchised dealers, Cox Automotive noted that a lack of new-vehicle inventory and no quick fix in the making is likely weighing on franchised dealers’ minds.

On the used-vehicle side, Cox Automotive discovered the inventory level index increased slightly as well in Q3 2022 to 36, one point higher than the previous quarter and up five points year over year.

Among franchised dealers, the used-vehicle inventory level index improved by 12 points year over year in Q3 to 47. The index was flat quarter over quarter for independent dealers.

The used-vehicle inventory mix index was also generally flat quarter-over-quarter and year-over-year at 47.

Still, Cox Automotive pointed out that all index scores associated with inventory remain below the 50 threshold, indicating dealers still face significant inventory challenges for both new and used vehicles.

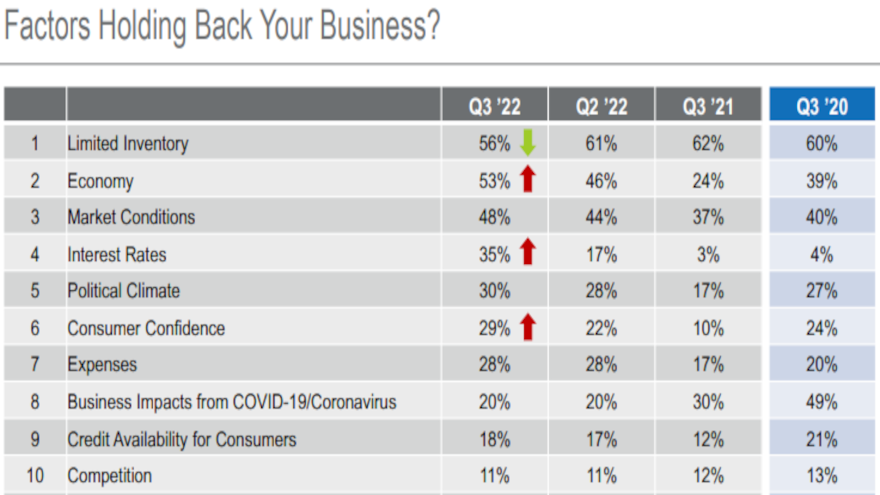

Consistent with last quarter, analysts determined limited inventory ranked as the No. 1 factor holding back dealer business in Q3.

While new-vehicle inventory sentiment improved in Q3, Cox Automotive mentioned the view of new-vehicle sales worsened slightly, decreasing from 52 to 51, meaning dealers are now marginally less optimistic about the current new-vehicle sales environment.

One year ago, the index score was also 51, meaning the same number of dealers saw the market as good versus poor, according to analysts.

The new-vehicle incentives index rose by one point quarter-over-quarter to 22 and has remained relatively stable in the low-to-mid-twenties for a year. For comparison, the incentive index was at 48 in Q3 2019.

Cox Automotive indicated the used-vehicle sales index remained stable at 47 in Q3.

For franchised dealers, the used-vehicle sales index decreased by three points and is now 12 points below year-ago levels.

For independent dealers, the index fell one point from the previous quarter to 41 and is down 13 points from a year ago.

“Overall, most dealers view used-vehicle sales as poor,” Cox Automotive said.

Economy & costs worry dealers

While limited inventory continues to be the top factor holding back business according to the Q3 2022 CADSI, analysts said factors tied to the economy and inflation are clearly causing concern with the dealers.

In Q3, Cox Automotive discovered the economy index dropped to 45, down from 50 in Q2 and 51 a year earlier. Cox Automotive explained this trend indicates more dealers see the U.S. economy as weak.

The economy, in fact, is the second leading factor impacting dealer business, with 53% of dealers citing it, up from 46% in Q2, with market conditions, interest rates and political climate following closely behind.

“Dealers are worried about inflation, the possibility of a recession and lagging consumer confidence,” Cox Automotive said, adding that in response to a new question, dealers indicate that inflation had a strong impact on every aspect of the dealership, including costs/expenses (80), interest rates (71), vehicle sales (62), fixed operations (62) and staffing levels (50).

Analysts also mentioned the cost index — specifically the cost of running a dealership — dipped one point to 75 in Q3 from the record high level in Q2 but remain historically elevated.

After reaching a record low in Q2 2020 of 51 at the height of the pandemic, Cox Automotive said the cost index has been steadily increasing.

Cox Automotive Dealer Sentiment Index methodology

The Q3 2022 CADSI is based on 1,040 U.S. auto dealer respondents, comprising 574 franchised dealers and 466 independents.

The survey was conducted from July 26 to Aug. 9.

Dealer responses were weighted by dealership type and sales volume to represent the national dealer population. For each aspect of the market surveyed, respondents are given an option related to strong/increasing, average/stable, or weak/decreasing, along with a “don’t know” opt-out.

Indices are calculated by creating a mean score in which:

—Strong/increasing answers are assigned a value of 100.

—Average/stable answers are assigned a value of 50.

—Weak/declining selections are assigned a value of 0.

—Respondents who select “don’t know” for a particular question are removed from the related index calculation. The total metrics reported have a plus/minus 3.0% margin of error.

The entire CADSI report can be found via this website.